The natural diamond market in April 2025 revealed significant pricing trends across clarity and color categories, shaped by supply chain shifts, evolving consumer demand, and competition from lab-grown diamonds. This month’s data highlights both resilience and challenges across premium, mid-range, and lower-tier diamond grades.

Premium Grades

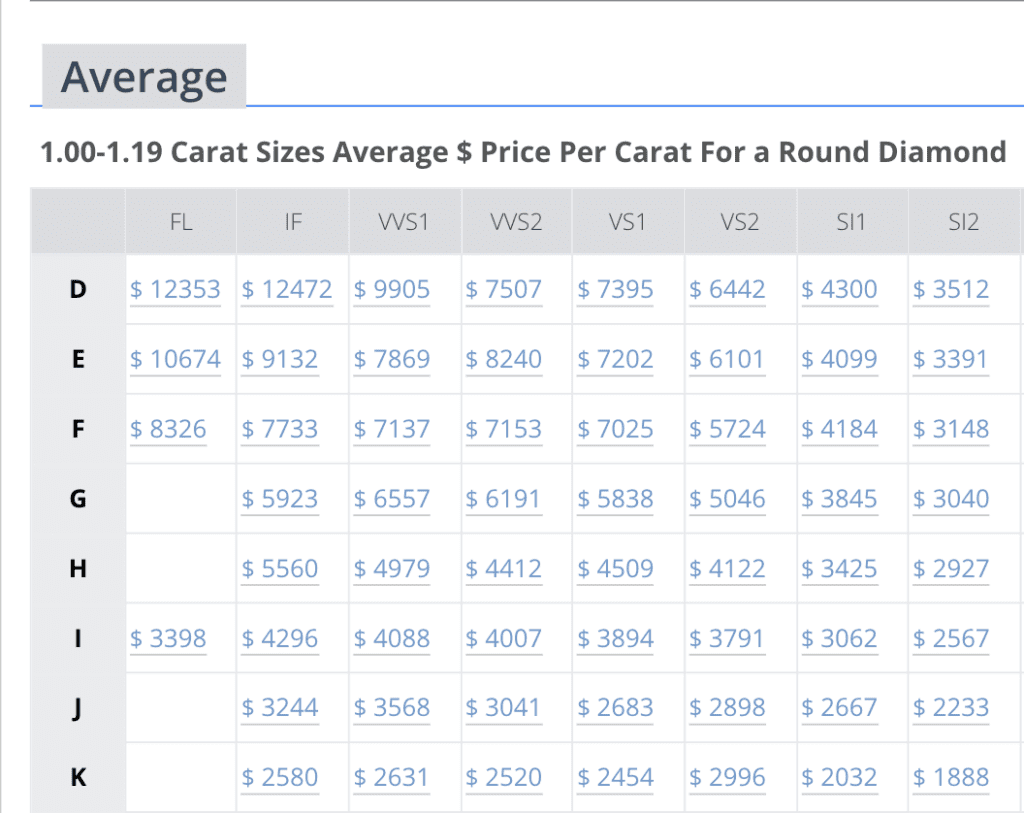

The upper-tier diamond categories experienced mixed movements, with some clarity grades showing resilience while others faced downward pressure. D/FL clarity diamonds saw a slight increase, rising from $12,092 in March to $12,353 in April, indicating a renewed interest in flawless diamonds, possibly driven by seasonal demand or a shift in high-net-worth consumer sentiment. D/IF clarity diamonds, however, declined slightly, dropping from $13,770 in March to $12,472 in April, signaling a softening in demand for internally flawless stones. This could reflect cautious spending among affluent buyers or competition from alternative investment options. E/FL clarity diamonds also experienced growth, increasing from $10,439 in March to $10,674 in April, suggesting sustained interest in high-quality diamonds within this color grade. These trends highlight a polarization in premium categories, with selective grades benefiting from targeted consumer demand while others face headwinds.

Mid-Range Grades

The mid-range clarity and color categories, often popular among PriceScope’s audience, demonstrated varying dynamics. F/VVS1 clarity diamonds remained stable, with prices moving slightly from $8,507 in March to $8,326 in April, reflecting consistent demand in this segment. G/VVS2 clarity diamonds, which saw a significant increase in March, faced a slight decline in April, dropping from $6,187 to $6,191. This marginal change suggests a plateau in demand following March’s surge. H/VS1 clarity diamonds showed a modest decline, falling from $4,735 in March to $4,509 in April, indicating potential inventory adjustments or a shift in consumer preferences toward other clarity grades. The mid-range segment continues to reflect strategic buying patterns, with consumers prioritizing value-focused options while remaining selective about specific clarity and color combinations.

Lower Grades

The lower-tier clarity and color categories remained under pressure in April, with a few exceptions. J/SI1 diamonds, which experienced a slight recovery in March, saw further stabilization, moving from $2,281 to $2,233. This suggests a continued, albeit modest, improvement in demand for budget-conscious stones. K/SI2 diamonds, however, declined further, dropping from $1,890 in March to $1,888 in April, underscoring the ongoing challenges in the lower end of the market. This decline is likely exacerbated by the growing appeal of lab-grown diamonds, which offer competitive pricing and perceived ethical advantages. The lower-tier segment remains the most vulnerable to competitive pressures from lab-grown alternatives and shifts in consumer priorities, particularly among cost-conscious buyers.

Market Implications

The April 2025 natural diamond market trends reveal a complex and evolving landscape. Premium categories, while stable, show signs of softening in certain high-clarity grades, suggesting a cautious approach among high-end buyers. Retailers should focus on targeted marketing to sustain interest in premium options. The mid-range segment continues to exhibit relative stability, with selective price fluctuations highlighting strategic consumer behavior. This segment remains a key area of opportunity for retailers seeking to capture value through competitive pricing and inventory optimization. Lower-grade diamonds face persistent challenges, driven by lab-grown competition and shifting consumer preferences. Retailers should monitor these trends closely and consider diversifying their offerings to include lab-grown options or value-focused natural diamonds.

Popular Diamond Shapes

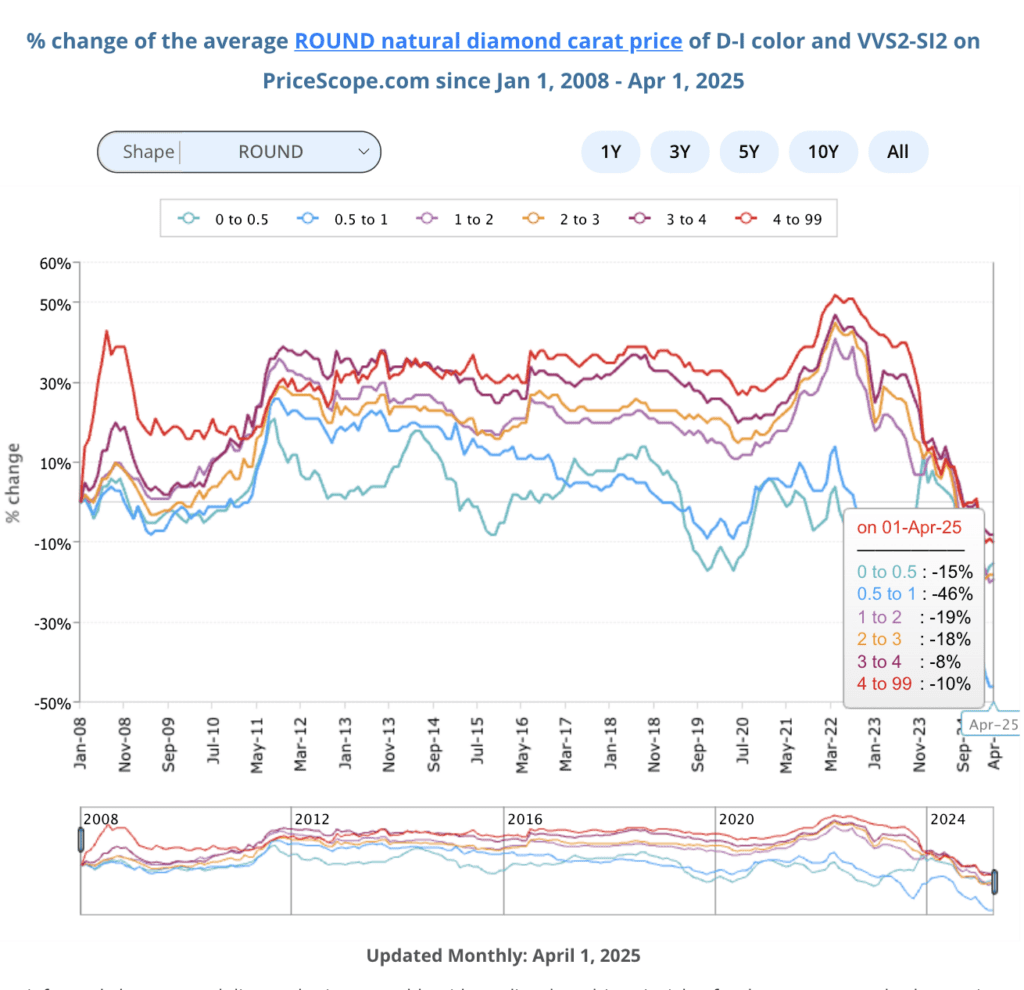

is an easy tool that analyzes the data of round diamonds and calculates a score that grades cut quality.")