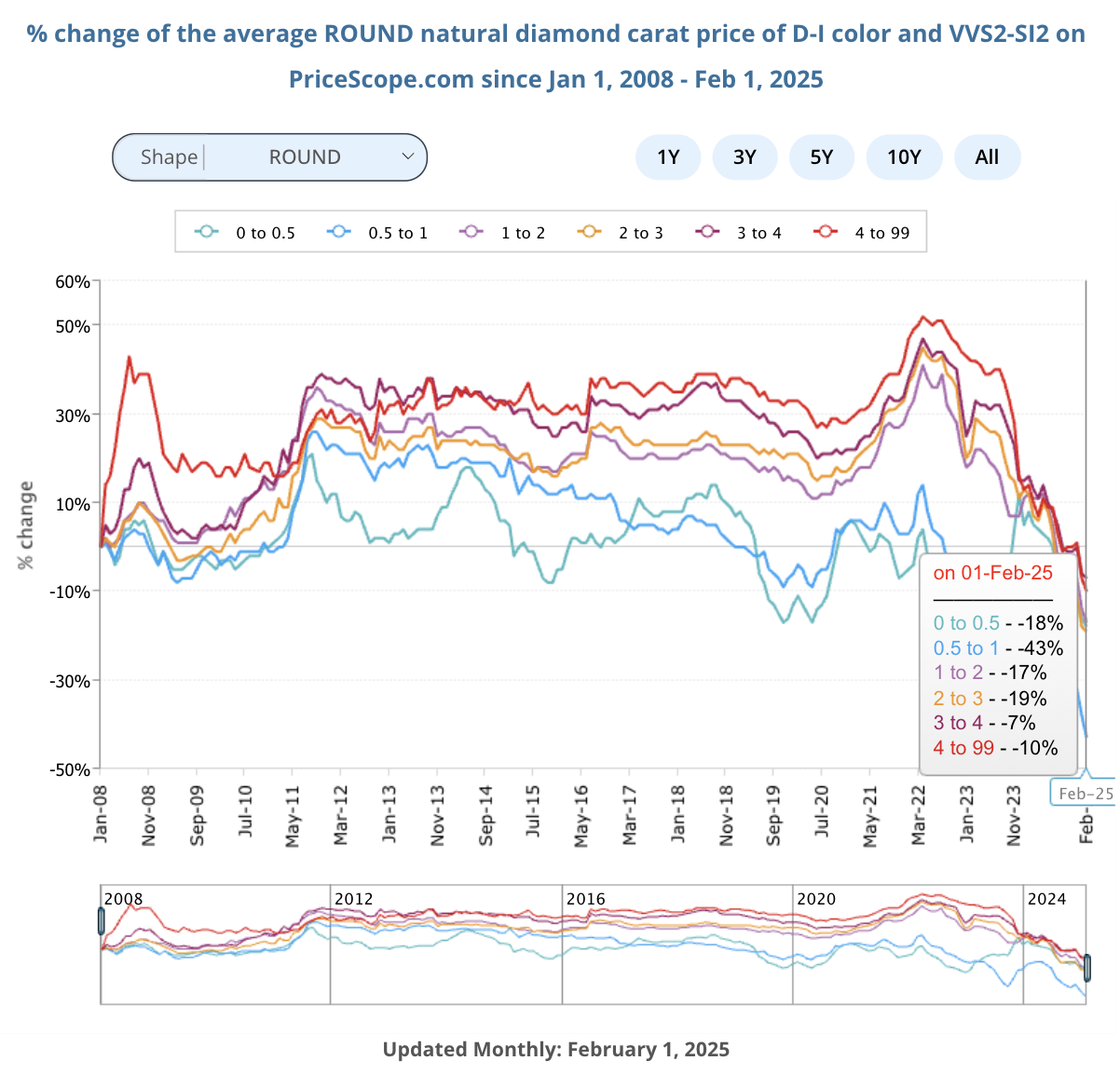

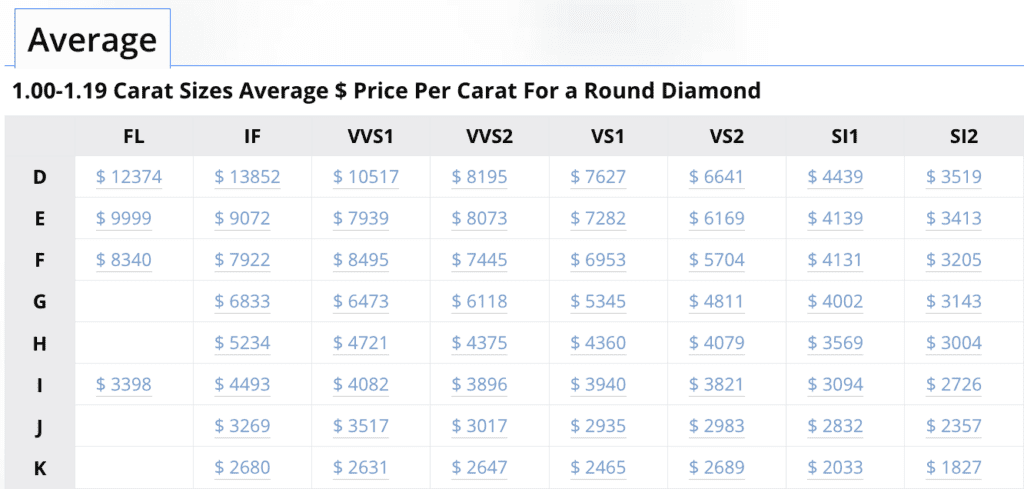

In February 2025, the natural diamond market for round diamonds in the 1.00–1.19 carat range demonstrated intricate pricing adjustments across multiple clarity and color categories. These fluctuations, analyzed in our latest diamond pricing report, reflect nuanced shifts in supply-demand equilibrium, investor sentiment, and evolving consumer preferences, further shaping the trajectory of the natural diamond market.

Premium Grades

The D color, FL clarity segment experienced a slight increase, rising from $12,351 in January to $12,374 in February. While this indicates continued demand for top-tier, flawless diamonds, the modest growth suggests a stabilization following the early-year surge.

Similarly, D/IF clarity diamonds rose from $13,468 in January to $13,852 in February, reflecting steady interest in internally flawless diamonds within this category.

Mid-Range Grades

The mid-range categories exhibited mixed price movements. F color, VVS2 clarity diamonds declined from $7,517 in January to $7,445 in February, reflecting a slight dip in demand for high-clarity diamonds in this tier. Conversely, G/VVS2 clarity diamonds saw a modest increase from $6,053 in January to $6,118 in February, suggesting selective purchasing trends and strategic buying at this grade level.

Lower Grades

The SI clarity segment continued to experience price pressure, particularly in the lower color grades. J/SI1 diamonds declined from $2,641 in January to $2,357 in February, reflecting ongoing softness in demand for budget-conscious stones possibly as a result of consumers making side by side comparisons with lab-grown diamonds. K/SI2 diamonds dropped further to $1,827, emphasizing continued market recalibrations at the lower end.

Market Implications

The February 2025 trends reinforce a stabilization in premium diamonds, with D/IF and D/FL categories holding strong amid steady high-net-worth investment. The mid-range segment remains fluid, with certain clarity grades showing resilience, while lower-tier diamonds continue to decline, likely reflecting competition from lab-grown alternatives and a cautious post-holiday retail environment.

As the natural diamond market navigates these trends, industry stakeholders should monitor evolving demand patterns, particularly in premium and mid-range categories, where strategic buying continues to shape price movements.

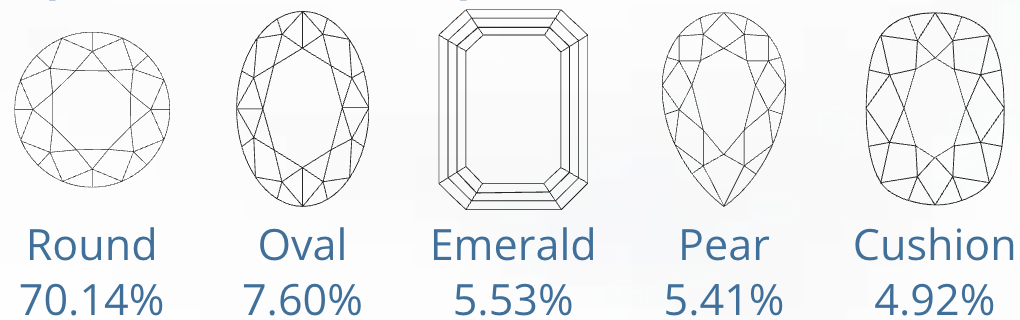

Popular Diamond Shapes

In our latest analysis of the Top 5 Popular Natural Diamond Shapes from January to February 2025, we’ve identified subtle yet telling shifts in consumer preferences, reflecting evolving trends in diamond purchasing behavior.

Round diamond continues to dominate the market, increasing slightly from 69.51% in January to 70.14% in February. This uptick of 0.63% suggests a sustained preference for the timeless brilliance of round diamonds, reinforcing their position as the go-to choice for buyers seeking optimal fire and brilliance.

Oval diamond, which surged in popularity in January, saw a 0.40% decline to 7.60% in February. While still maintaining its position as the second most popular shape, this dip might indicate a slight shift in demand as buyers explore other elongated or step-cut alternatives.

A notable movement within the rankings occurred between the Emerald and Pear shapes. Emerald cut edged ahead of the Pear cut, increasing slightly from 5.52% to 5.53%, overtaking the Pear shape, which declined from 5.64% to 5.41%. This reversal suggests a growing appreciation for the Emerald cut’s clean lines and sophisticated appeal, while demand for the Pear cut remains strong but slightly diminished.

Meanwhile, the Cushion cut continued its gradual decline, decreasing from 5.16% in January to 4.92% in February. This marks the second consecutive month of market share reduction, potentially indicating shifting consumer interest away from the softer, pillow-like faceting style in favor of more structured cuts.

These fluctuations highlight the dynamic nature of diamond shape preferences. While the Round cut remains unrivaled, fancy shapes continue to compete for consumer attention, with small but notable adjustments in demand. As the year progresses, industry stakeholders should monitor whether these trends stabilize or if we see further shifts in shape preferences influenced by new engagement ring trends, or broader market conditions.

When shopping for loose diamonds, it’s important to consider factors like cut quality and vendor services, such as upgrade options and return policies, which can significantly influence the price. At PriceScope, we’ve been tracking retail diamond prices since 2007, with over 1,200,000 diamonds currently in our database. Our Diamond Price Chart page, updated monthly, offers comprehensive price insights for both round and fancy-shaped diamonds. Be sure to check back for March 2025’s natural diamond price updates.

As February 2025 concludes, price adjustments indicate sustained interest in D/IF and D/FL diamonds, selective movement in VVS and VS categories, and continued softening in SI and lower-clarity grades. The reshuffling in shape preferences, with Emerald overtaking Pear, suggests evolving consumer priorities in faceting styles. These shifts underscore the importance of data-driven inventory and pricing strategies. We encourage you to share your insights or join the discussion by clicking the comments button below.

Latest Publications on Diamond Prices February 2025:

Rapaport

IDEX

The Guardian

is an easy tool that analyzes the data of round diamonds and calculates a score that grades cut quality.")